"RAB

has been concerned with auditor independence since

well before the Enron collapse focused attention on

the inherent conflict of financial accounting firms

providing clients with both consulting and auditing

services. The management systems community has taken

the high road by insisting on a clear separation of

auditing and consulting activities. This stance was

taken to ensure impartiality and freedom from conflict

of interest in management systems auditing."

--Bob King,

president and CEO of Registrar Accreditation Board

|

Why have so few companies registered

to ISO 9001:2000? In its July 2002 ISO 9000 survey, Quality

Digest reported "the actual figure [of companies

that have transitioned] is probably 8 to 10 percent."

Companies now have barely more than a year to change to

the new standard. One major reason for the slow response

might be that ISO 9001:2000's perceived value isn't sufficiently

compelling in these slow economic times.

One solution for easing the transition to ISO 9001:2000

is to conduct value-added audits. What is value-added auditing?

According to the Institute of Internal Auditors' Web site

(www.theiia.org), it's

"a systematic, disciplined approach to evaluate and

improve the effectiveness of risk management, control and

governance processes." Value-added auditing is so hot

that the New York Stock Exchange and the Securities and

Exchange Commission now require value-added audits of more

than 17,000 listed companies.

It's no exaggeration to say that dramatic changes have

occurred recently in business. Enron, WorldCom and a number

of other companies have collapsed. The U.S. government has

passed laws requiring financial disclosure. And on Aug.

1, 2002, the New York Stock Exchange began requiring all

its listed companies to have an internal audit function.

There have been many changes in the quality world as well.

Companies are transitioning to a major standard revision:

ISO 9001:2000. The Registration Accreditation Board, which

certifies quality and environmental management systems auditors,

strengthened its policies regarding consulting and auditing

independence.

Quality auditors and internal auditors have noticed a

new emphasis on analytical auditing that involves process

audits, risk and/or control assessments, and other forms

of effectiveness assessments. Generally, this trend is called

value-added auditing.

Why should quality auditors and the rest of us in the

quality profession pay attention to value-added auditing?

We're now officially in a recession, and senior managers

don't want surprises. They and their boards of directors

are thinking, "Do we have sufficient information and

assurance of operational effectiveness internally, as well

as with our supply partners, to make robust decisions?"

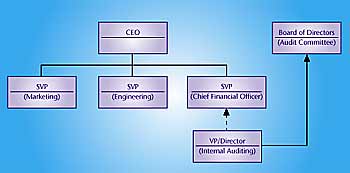

Internal auditing departments are responsible for conducting

value-added audits. Because of recent legislation concerning

corporate governance, these reports often go directly to

the board of directors' audit committee and indirectly to

the chief financial officer. (See Internal Auditing Reporting

Relationship.)

Steve Jameson, the Institute of Internal Auditors' director

of technical services, recently had this to say about the

new regulations coming out of Congress, the SEC and the

NYSE: "Requiring public reporting on internal controls

is the grand prize that the internal audit profession has

sought for years. The U.S. Congress has now mandated that

requirement. The IIA standards and the IIA's value-added

mindset for the profession support and promote internal

auditors as the key organizational resource for providing

assurance about internal controls to the [board of director's]

audit committees and management."

Our quality audits go directly to a first- or second-level

manager. But as quality professionals, we want to make a

difference with our quality reports. Will we be most effective

by conducting quality management system assessments that

go to a first-level manager, or will we add more value by

collaborating with internal auditing to provide consolidated

audit reports to the board of directors' audit committee?

The latter is the obvious choice.

All organizations exist to add value to their stakeholders.

But this elusive quality can mean different things to different

stakeholders. To shareholders, "value" means raising

the stock price. To senior management it means operational

effectiveness. To boards of directors, it means no surprises.

To regulatory authorities, value means compliance to laws.

In order to provide value, quality auditors should be

able to assess:

Operational and quality effectiveness

Operational and quality effectiveness

Business risks

Business and/or process controls

Process and business efficiencies

Cost reduction opportunities

Waste elimination opportunities

Corporate governance effectiveness

Many people think that internal auditing focuses primarily

on financial audits. The Institute of Internal Auditors

developed a definition of auditing that introduces various

elements of value-added auditing:

"Internal auditing is an independent, objective assurance

and consulting activity designed to add value and improve

an organization's operations. It helps an organization accomplish

its objectives by bringing a systematic, disciplined approach

to evaluate and improve the effectiveness of risk management,

control and governance processes."

We can infer a number of value-added auditing "best

practices" from that definition. Value-added audits

aim to:

Provide independent and/or objective operational analysis

Examine every function, process and activity of an organizational

and external value chain

Help an organization achieve its business strategies and

objectives

Follow a systematic and disciplined approach in its assessment

Evaluate and improve the effectiveness of risk management,

control and governance processes

Quality and internal auditing are converging around the

theme of value-added auditing. The RAB and leading ISO standards

registrars are spearheading the drive to provide higher

levels of transparency, assurance and, ultimately, value

to quality audit reports.

North America's top registrars are also emphasizing value.

"With today's stock market volatility, investors want

higher assurance of company performance," says Tom

Harris, managing director of AOQC Moody International. "Quality

auditors must evaluate management systems and processes

not only in terms of compliance to a standard but, most

important, to analyze their effectiveness. Companies must

develop mission-critical objectives and then hold process

owners accountable for the measurement, control, analysis

and improvement of their systems and processes. AOQC Moody

International is rapidly moving in this direction."

"Last May, RAB's Auditor Certification Board approved

new language on auditor independence for all RAB auditor

certification programs," says Bob King, president and

CEO of RAB "Specifically, there must be a period of

at least two years between any consulting an auditor does

for an organization and any auditing he or she performs

for the same organization. As more is being said and written

on the topic of value-added auditing, we want to make sure

our auditors have a very clear sense of the line between

auditing and consulting."

Actually, quality auditors already conduct value-added

audits. Let's take a closer look at these, which include:

Compliance audits

Process audits

Risk assessments

Internal control assessments

Self-assessments

Consulting

The key elements of a compliance audit can be gleaned

from the

ISO 9001:2000 definition, which characterizes an audit

as a "systematic, independent and documented process

for obtaining audit evidence and evaluating it objectively

to determine the extent to which audit criteria are fulfilled."

Audit criteria, according to the same source, are a "set

of policies, procedures or other requirements against which

collected audit evidence is compared." Likewise, audit

evidence consists of "records, statements of fact or

other information relevant to the audit and which are verified."

Most of us are familiar with compliance audits through

ISO 9001 requirements. Fundamentally, they're documentation

reviews that result in a binary decision, i.e., compliance

or noncompliance. If there's noncompliance, then the auditor

will issue a corrective or preventive action request.

Compliance audits add value to governmental agencies and

to commercial organizations that mandate contractual or

regulatory compliance. They're probably the easiest audits

to conduct because the requirements are already written,

and less auditor discretion is required.

ISO 9001:2000's biggest compliance challenge is determining

how to conduct a process audit to demonstrate "effectiveness."

Most quality and ISO standards pundits think that an effectiveness

audit implies some type of process audit. Although there's

still confusion and little standardization about how to

conduct a plan-do-check-act process audit, the following

are practical steps:

1. Identify business objectives

2. Flowchart processes

3. Identify critical process inputs and outputs

4. Evaluate process procedures, records and documentation

against ISO 9001:2000 requirements

5. Evaluate process metrics against business objectives

6. Analyze metrics to determine process stability and capability

7. Improve performance through intervention and preventive

and/or corrective actions

In addition, process audits can go beyond evaluating the

effectiveness of ISO 9001:2000 quality management system

clauses and evaluate supply-chain processes against internal

business objectives and external business benchmarks.

As recently as five years ago, quality was the primary

filter through which U.S. senior management reached decisions,

and customer satisfaction was the critical quality attribute.

Then costs and schedules superseded quality as the primary

senior-management decision filter. Competing in an increasingly

aggressive business environment meant being first to market,

first to critical mass and paying attention to other time

elements.

Sept. 11 changed all that. Risk and its management is

now the primary filter by which management makes its decisions.

This is why risk audits will become more critical to organizational

operations.

The acronym ORCA is a common organizational risk-assessment

methodology. It requires that organizations:

Identify business objectives

Identify operational and other risks

Define business or other controls

Assess the effectiveness of the business process to satisfy

objectives and manage risks

Once this risk assessment is conducted, senior and operational

management can develop strategies to manage risks and execute

business decisions. Risk management strategies include:

Avoidance

Mitigation

Acceptance

Diversification

Control

The following excerpt from IBM's 1998 annual report illustrates

the importance and purpose of internal controls:

"IBM maintains an effective internal control structure.

It consists, in part, of organizational arrangements with

clearly defined lines of responsibility and delegation of

authority, and comprehensive systems and control procedures.

To assure the effective administration of internal control,

we carefully select and train our employees, develop and

disseminate written policies and procedures, provide appropriate

communication channels, and foster an environment conducive

to the effective functioning of controls."

Internal control is the fundamental idea underlying the

entire financial and operational structure of the organization--as

indicated by IBM's chairman of the board and chief financial

officer signing the statement.

According to the Committee of Sponsoring Organizations

of the Treadway Commission's Web site (www.coso.org), internal

control is a process designed to ensure reasonable confidence

regarding:

Effectiveness and efficiency of operations

Reliability of financial reporting

Compliance with applicable laws and regulations

Internal control assessments evaluate these five interrelated

elements of effectiveness and value:

Control environment. Senior management sets the tone for

vision, mission, quality, ethics, goals and controls. Daily

operational control defers to the people who know the process

or product--i.e., the process owners.

Risk assessment. Risk management will be the fundamental

objective of all managers during the next few years. The

preconditions to effective risk management are identified

as core processes, stabilized processes, capable processes

and controlled process variations.

Control activities. These include the people, policies,

suppliers and other factors that ensure risks are identified,

monitored and mitigated throughout the project, product

or contract lifecycle. Controls may include approvals, authorizations,

validation, verification, reconciliation and segregation

of authorities.

Information and communication. No information and no communication

mean no control. It's that simple.

Monitoring. Internal controls systems and processes must

be monitored. It's not enough to recognize that a process

is out of control--or worse, noncompliant with a specification

or standard. Ongoing monitoring, says COSO, should ensure

corrective and preventive actions.

The workplace modus operandi is moving toward self-managed

work teams. Chances are you may be in one or several. Self-managed

teams comprise self-directed individuals who accept responsibility

for developing schedules, managing quality, controlling

costs, upgrading worker skills, assigning work, improving

process performance, focusing on results and ensuring that

stakeholders are satisfied. Multijob classifications are

replaced by one-worker classification. The work environment

is open and friendly. Time clocks are eliminated. Compensation

is based on pay-for-knowledge, i.e., people are paid on

the basis of training, experience, knowledge and value-addition.

Workers and process owners are responsible for managing

risks and controlling their processes.

Self-managed teams and individuals can assess the value

of their work through:

Balanced scorecards

Checklists with ratings

Internal control questionnaires

Team-written procedures and instructions

Process control information such as SPC

Senior management and an organization's board of directors

are responsible for risk management and operational control

processes. However, value-added auditors can also serve

as consultants to assist the organization in identifying

improvement opportunities, evaluating risks and implementing

risk-management methodologies and controls. This is a major

change in internal and other auditing disciplines, where

it was assumed that an unassailable firewall stood between

the auditor and auditee.

Traditionally, auditors were independent and objective.

Independence implied that an arms-length relationship existed

between the auditor and auditee. If the auditor provided

the auditee with consulting assistance, the prevailing belief

held that the auditor's independence might be impaired,

although his or her objectivity to the auditee still provided

value. The notion of auditor as consultant represents a

major change in the Institute of Internal Auditing standards

as quality and internal auditors evolve into "business

process" assurance and consulting experts.

ISO 9001:2000 now requires "effectiveness" and

process auditing. But how does a quality auditor audit for

effectiveness? This is a challenge for all quality auditors,

ISO standards registrars and quality consultants. The solution

is to perform some form of value-added auditing.

Quality auditors can transition to value-added auditing

as long as it's done carefully. Several issues must be understood

and addressed:

Open to interpretation. Evaluating effectiveness, risk management

and internal controls varies according to how the standards

and/or processes are interpreted.

Inconsistent application. Evaluating effectiveness, risk

management and internal controls can vary among auditors.

Requires additional auditor skills. Value-added auditing

requires profound business, process and people knowledge.

Possibility of additional variation. No consistent and well-established

standards and protocols exist for conducting value-added

audits.

Compliance regulatory audits won't disappear. Indeed,

they add value through regulatory assurance. However, all

boards of directors of publicly held companies want additional

information and assurance beyond a yes/no decision. They're

asking auditing and assurance services to evaluate risk

management and operational control effectiveness.

Many quality gurus think that value-added auditing will

be the profession's future. "Value-added auditing is

auditing for increased profitability and improved customer

satisfaction," says Jim Lamprecht, consultant and author

of ISO 9001-related books.

So, what does our quality-auditing crystal ball reveal

of our profession's future?

Consolidated quality audit and internal audit reports will

go to the board of directors.

The quality auditing function will integrate with internal

auditing.

The term "quality audit" will fade from ISO standards'

vocabularies.

Multiple audits will be conducted for different stakeholders.

Compliance and regulatory systems assessments will still

be conducted.

Quality auditors will emerge as value-added auditors and

business process consultants.

Value-adding auditing as a tool will increase exponentially.

Auditor training requirements will increase.

Quality auditing needs more exposure. Many compliance

and ISO 9000 audits end up with first-level managers for

subsequent action. In turn, the Institute of International

Auditing definition of auditing has shaped value-added auditing.

These internal audit reports ultimately end up with the

board of directors' audit committee. This is where we want

our quality audit reports to reside. It's up to us to work

with internal auditing to develop consolidated quality,

customer-supply, risk and control audit reports.

Greg Hutchins, PE, is a management principal with Quality

Plus Engineering, a Portland, Oregon-based risk, process,

project and supply management company. He can be reached

at (800) 266-7383 or www.valueaddedauditing.com.

Hutchins has written more than 15 books, including his most

recent, Value Added Auditing, from which this article was

excerpted. Letters to the editor regarding this article

can be sent to letters@qualitydigest.com.

|